Stata? I Only Know Python

Contents

![]()

Stata? I Only Know Python#

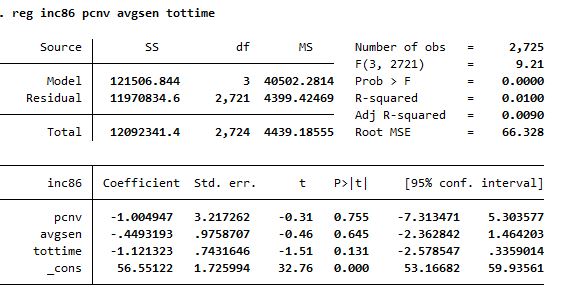

The idea of this class is to mimic the typical output of a Stata least squares regression.Below you can see an example of the output of a regression of this type in Stata using the ‘crime1’ database from the Wooldrige Econometrics book.

Excuting the comand reg inc86 pcnv avgsen tottime the output is:

¡Time To Create!#

As I mentioned before, the idea is to create a class that allows us to replicate Stata output in python. So let’s do it!

# We have to import some modules to use matrix and calculate statistics

import numpy as np

import pandas as pd

import scipy.stats as sst

from scipy import stats

class Lineal_Reg(object):

def __init__(self,Y,X,alpha=0.05,intercept = True):

self.intercept = intercept

self.Y = Y.to_numpy().reshape(len(Y),1)

if self.intercept == True:

self.X = np.c_[np.ones(self.Y.shape[0]),X.to_numpy()] if len(X.shape) !=1 else np.c_[np.ones(len(X)),X.to_numpy().reshape([len(X),1])]

elif self.intercept == False:

self.X = X.to_numpy() if len(X.shape) !=1 else X.to_numpy().reshape([len(X),1])

self.alpha = alpha

self.names = X.columns if len(X.shape)!=1 else [X.name]

self.n = self.X.shape[0]

self.k = self.X.shape[1] -1 if len(X.shape) !=1 else 1

self.gl = self.n - self.k -1

class fit():

def __init__(self):

Lineal_Reg.__init__(self,Y,X,alpha=0.05,intercept = True)

self.betas = (np.linalg.inv(self.X.T@self.X)@self.X.T@self.Y)

def __anova(self):

self.residuals = self.Y - (self.X @ self.betas)

self.SEC = np.sum(np.square(self.X @ self.betas -np.mean(self.Y)))

self.SRC = np.sum(np.square(self.residuals))

self.STC = np.sum(np.square(self.Y-np.mean(self.Y)))

self.R_2 = 1-self.SRC/self.STC

self.statistic_F = (self.R_2 / self.k) / ((1-self.R_2)/(self.n - self.k -1))

self.MS_model = self.SEC / self.k

self.MS_residual = self.SRC / self.gl

self.MS_total = self.STC / (self.n - 1)

def __table_results(self):

self.m_covariances = (self.SRC/self.gl) * (np.linalg.inv(self.X.T @ self.X))

self.variances = np.diag(self.m_covariances)

self.standard_error = np.sqrt(self.variances).ravel().tolist() # ya quedo en lista

self.t_values = [betas/errors for (betas,errors) in zip(self.betas.ravel().tolist(),self.standard_error)]

self.p_values = [stats.t.sf(np.abs(t_val), self.n-1)*2 for t_val in self.t_values] #t,Gl

#intervals

self.t_level = sst.t.ppf(1 - self.alpha/2, df=self.n - self.k - 1 ) # df = n-k-1

self.intervals = [sorted([beta - (errcoef * self.t_level),beta + (errcoef * self.t_level)]) for (beta,errcoef) in zip(self.betas.ravel().tolist(),self.standard_error)]

@property # decorator to turn a method in an attribute

def summary(self):

self.__anova()

self.__table_results()

panel = pd.DataFrame(index=['Model','Residuals','Total'])

panel['SS'] = [round(i,2) for i in [self.SEC,self.SRC,self.STC]]

panel['df'] = [self.k,self.gl,self.n-1]

panel['MS'] = [round(i,2) for i in [self.MS_model,self.MS_residual,self.MS_total]]

panel[' '] = [' ',' ',' ']

panel[' '] = [f'No. Observations = {self.n}',f'F{self.k,self.gl} = {round(self.statistic_F,2)}',f'R-squared = {round(self.R_2,4)}'] # Esto toca organizarlo mejor

results=pd.DataFrame(index= ['_Cons']+ [i for i in self.names]) if self.intercept == True else pd.DataFrame(index= [i for i in self.__names])

results['Coefficients'] = [round(i,3) for i in self.betas.ravel().tolist()]

results['S. Error'] = self.standard_error

results['t'] = [round(i,2) for i in self.t_values]

results['P'] = [round(i,4) for i in self.p_values]

results['Confidence Intervals'] = [(round(i[0],6),round(i[1],6)) for i in self.intervals]

print(panel)

print()

print(results)

¡Time To Test!#

Now using the wooldridge python package we can try to execute the same regression model with our class and compare the results

import wooldridge as wd # Dont Forget to install wooldridge package

df = wd.data('crime1')

Y = df['inc86']

X = df[['pcnv','avgsen','tottime']]

model = Lineal_Reg(Y,X,alpha=0.05) # Creating the object

reg = model.fit() # using fit method

reg.summary # Using summary attribute

SS df MS

Model 121506.84 3 40502.28 No. Observations = 2725

Residuals 11970834.58 2721 4399.42 F(3, 2721) = 9.21

Total 12092341.43 2724 4439.19 R-squared = 0.01

Coefficients S. Error t P Confidence Intervals

_Cons 56.551 1.725994 32.76 0.0000 (53.166824, 59.935609)

pcnv -1.005 3.217262 -0.31 0.7548 (-7.313471, 5.303577)

avgsen -0.449 0.975871 -0.46 0.6452 (-2.362842, 1.464203)

tottime -1.121 0.743165 -1.51 0.1315 (-2.578547, 0.335901)

Let’s Talk A Little About What We created …#

The class is mainly composed of two parts, the first is an initiator function __init__() where the first attributes of the object are created and manipulated, which in this case will be the arrays of dependent and independent variables according to the regression. Apart from this initiator function, a class called fit() is created within our first class, the idea is that this is started and the calculation of the betas will be executed, however it is saved and can be accessed using the method converted to summary attribute, which generates all the output with the help of other methods generated within the same subclass. Methods such __anova() and __table_results are hidden to the users, they only work inside the class, we can do thath usgin Methods such __anova() and __table_results are hidden to the users, they only work inside the class, we can do that using __ before the name of a method.

Some Conclusions …#

The main conclusion that stands out from this project is that the open source philosophy and technologies allow us to develop thousands of ideas, codes and applications that some companies would sell. In my case I have the Stata17 license because my university pays for it, however using python I was able to replicate one of the most popular outputs for students of basic econometrics courses.